SHI 12.11.19 – Folks are Working!

SHI 12.4.19 – The Issue of Unintended Consequences

December 4, 2019

SHI 12.18.19 – Goodbye to an Exciting Year

December 18, 2019

“The final employment reading for 2019 showed 3.5% unemployment … “

… and trumpeted the fact that 266,000 jobs were added to our civilian labor force during November. This was a blowout number … completely unexpected by the press and forecasters alike. Me too. Frankly, I was shocked by the size of the number. So I decided to dig in a bit deeper and make sure the reality of the employment situation was as good as the headline promised.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Make no mistake: People ARE working. Don’t let all the rhetoric around minimum wage, wealth inequality, compensation growth rates, etc, fool you … people are working. In fact, more than ever! This is purely a quantitative comment. I am making no qualitative inferences here. My statement is purely mathematical, and it is accurate.

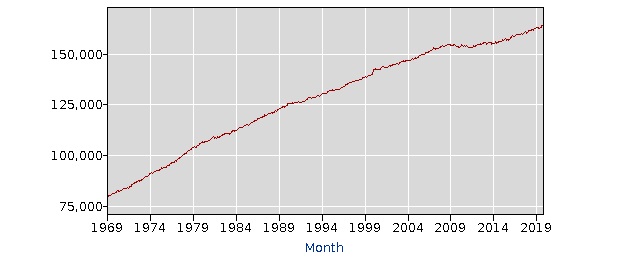

Never before in the history of America has today’s number of people held jobs. To the right is a chart courtesy of the United States Bureau of Labor Statistics (BLS), showing the size of the ‘Civilian Labor Force’ (the CLF) over the past 50 years. It’s easy to see the red line has moved up, up, UP almost continuously. The rate of growth has slowed lately (post-2008 recession), but growth continues.

Back in January of 1969, the CLF had 79.5 million folks in its ranks. In November of 2019, this number had grown to 164.4 million — more than double. All other factors aside, the growth here is impressive.

And a 3.5% unemployment rate is also very impressive. Again, setting all qualitative comments aside, we haven’t seen an unemployment rate this low for about 50 years. 1969 was the last time the US experienced an unemployment rate of only 3.5%.

Of course, 1969 was a long time ago … and much was different back then. For example, the Q1, 1969 GDP growth rate was a staggering 9.23%! By Q4 this had fallen to 7.3%, and shortly thereafter the 1970 recession began. Interestingly enough, at the depths of that recession, US GDP was still growing at an annual rate of 4.8%. Yes, there were very different times. I would LOVE to see a 4.8% GDP growth rate today at the peak of an economic expansion! Let alone at the bottom of the trough.

As my long-time readers know, unfortunately I believe those lofty levels of GDP growth rates are far in our rear-view mirror. Today, I’d be thrilled with a 3% annual growth rate, but I suspect even that level is unattainable on a sustained basis. More on this topic later. Let’s get back to the employment numbers.

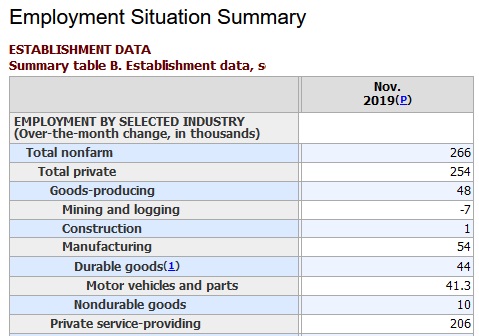

Opening the supporting charts in the latest employment situation, specifically ‘Summary Table A’ we see that during November the CLF grew by only 40 thousand folks. Hmmm…this is odd, inasmuch as the economy added 266,000 new jobs. If 266,000 new jobs were added to the economy, how can this be accurate?

The answer is a bit murky. On one hand, as we see in the chart to the right, 266 thousand new jobs were created. Per the BLS, this is factual.

On the other hand, Table A-1 tells us that in addition to the CLF growing by 40,000 during November:

- The number of people actually employed increased by only 83 thousand.

- The employment to population ratio was unchanged at 61%

- Folks who are now “not in the labor force” increased by 135,000.

So, summarizing, it appears that while the CLF grew only slightly, the majority of the 266,000 new jobs were absorbed by people who were previously in the ranks of the unemployed, even as 135,000 more people left the labor force. (Think retirees.)

Confusing, I know.

Here’s the bottom line: At this stage of our economic expansion, our economy is showing amazing resiliency. The FED rate cuts appear to have done the trick. For now.

In fact, the FED just finished their last 2-day 2019 meeting and then released this statement:

“The Committee decided to maintain the target range for the federal funds rate at 1‑1/2 to 1-3/4 percent. The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective. The Committee will continue to monitor the implications of incoming information for the economic outlook, including global developments and muted inflation pressures, as it assesses the appropriate path of the target range for the federal funds rate.”

So, interest rates remain unchanged.

The inverted yield curve that had us all so worried seems to have floated off into temporary obscurity … employment levels have continued to increase … and our GDP growth seems to be chugging along. Folks are working … and steaks are selling.

So, for now, we can take comfort from the fact that the machinery here in the US economy, as a whole, seems to be working as it should. On a quick aside, this is not the same in Europe, Japan or England The engines of these economies are struggling. Christine Lagarde takes the helm of the European Central Bank today. This is her greatest challenge. In all 3 cases, central bankers and politicians are discussing fiscal stimulus to juice up their economies. In other words, all 3 are debating increasing their country’s debt levels, and then using the new debt to fuel expenditures designed to rev up their economies. More on this later.

But here at home, while our engine is still chugging along on 5 or 6 cylinders, it is chugging along. And it will continue to do so until it doesn’t. Prophetic, right? 🙂

Here’s what I mean. Take a look at the chart below:

First, note the horizontal red line I drew at the bottom of the graph. One must travel back 50 years in time, to 1969, to find a match for today’s 3.5% reading for the unemployment rate.

But soon thereafter, things change. The 5 red arrows I’ve added in each case show a rapid increase in the unemployment rate in the months following the bottom of the trough. Each of these episodes corresponds with significant job losses due to a spreading economic contraction. And while the causes for each of the contractions in 1970, 1980, 1982, 1990, 2003 and 2008 were unique, in all cases jobs losses were significant. The unemployment rate increased significantly … and many folks were no longer working.

When will this current expansion cycle end … and the rise in unemployment repeat? No one knows. We only know that it will. Which is why its so important to keep our eyes glued to, and our fingers on the pulse of, the Steak-House Index! Yes, you are right, this is a shameless plug to be sure. But it’s true! 🙂

And what is the SHI10 telling us today?

IT’S A CHRISTMAS MIRACLE!

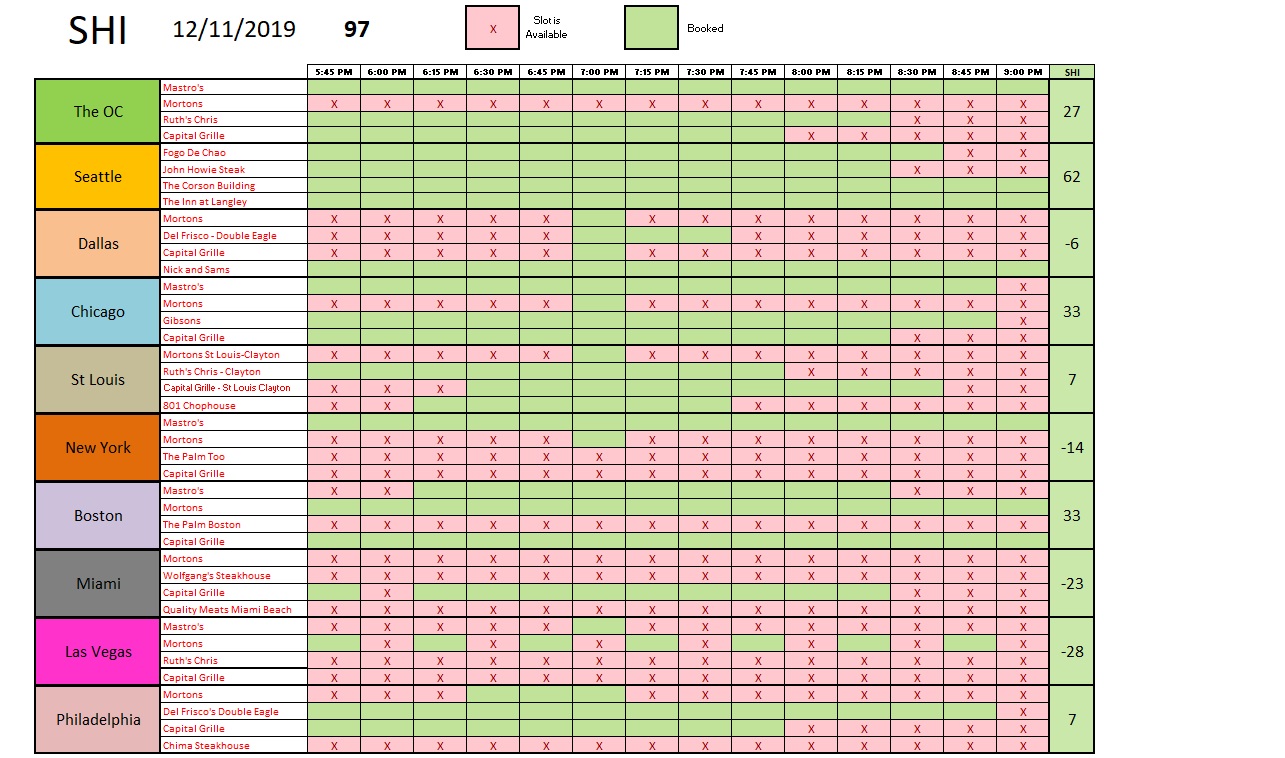

For the first time in ages, the SHI10 is positive! Look at all that green … there’s so much green, it reminds me of a Christmas tree:

Reservations for expensive eateries on the west coast are hard to come by this weekend. It’s interesting to see the same is not true in Dallas. I wonder what that’s about. And the rest of the country is a bit of a mixed bag. But make no mistake: The X-mas rush for pricey cuts of beef is on! If you want to visit your favorite steakhouse in the near future, you’d better make that reservation ASAP!

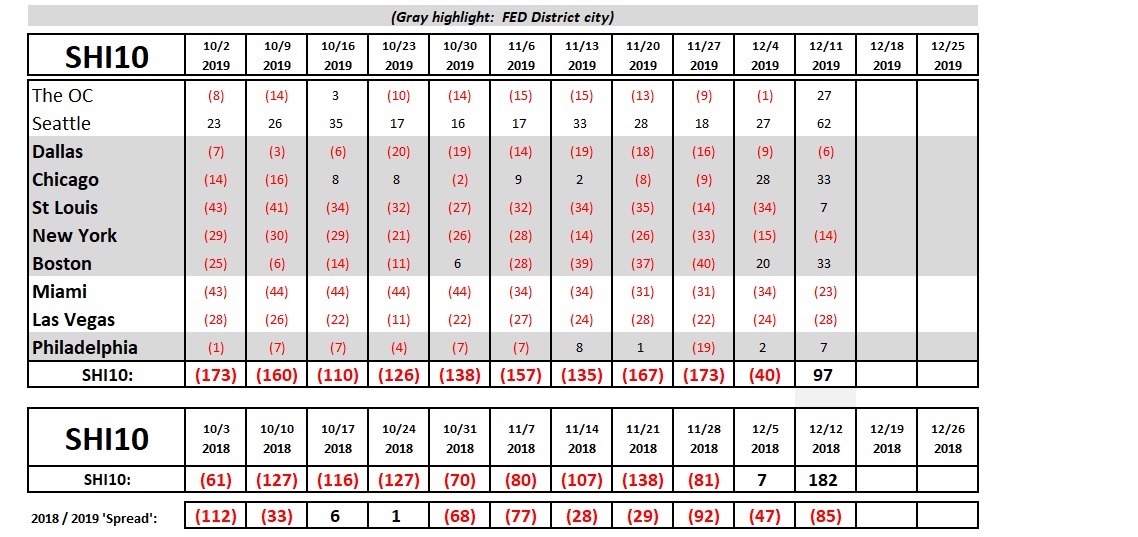

Here’s the longer term trend:

Yep, things are heating up for the Christmas season at our elegant steakhouses. Of course, last year’s SHI number was still better … but the fact that today’s reading is following the familiar pattern gives us comfort that the well-heeled consumer continues to feel flush. Good.

Let me finish with a brief comment on Paul Volcker. Mr. Volcker recently passed away. My younger readers may not know Mr. Volcker. Paul became the chairman of the FED in 1979, at a time when the US inflation rate was rampant and increases seemed unending. Something had to be done to stop this run-away train. And Mr. Volcker was the man to do it. While the policies he implemented caused plenty of hardship for many people, his efforts solved the problem … and, in my opinion, saved the US economy from even greater pain. This statement is contentious to be sure, and I’ll gladly debate it any time over a nice bottle of red wine. But for now, I’ll simply say good bye to a great man. There are not enough of them around these days.

Happy Holidays!

– Terry Liebman