SHI 11.20.19 A Tasty Visit to The Big Mac Index

SHI 11.13.19 King Consumer

November 13, 2019

SHI 11.27.19 – 400 Years Ago

November 27, 2019

“Be honest: Just looking at that picture, makes you hungry, right?”

The Big Mac is sold in more than 36,000 McDonalds restaurants in over 100 countries. That’s more than half the 190 countries that span the globe. This double-decker burger is made from only 7 ingredients and is nearly identical in every single case. This consistency, country after country, store after store, is what makes the Big Mac Index, The Economist’s “lighthearted guide” to currency valuation, possible.

Consistency. That’s the key. And, of course, the fact that the burger is constructed in more than 100 countries. So if a Big Mac costs less in Russia than here in the US — after converting the rouble into US dollars — then a likely conclusion, BMI theory holds, is that the rouble is undervalued. Wow … that’s a lot! Continuing this example, in January of this year, a Big Mac would set you back 110 roubles ($1.65), compared with $5.58 in America, suggesting the rouble is undervalued by 70% against the US dollar. At the same time, in Switzerland McDonald’s customers had part with SFr6.50 ($6.62) for that identical Big Mac, which implies that the Swiss franc is overvalued by 19%.

What does the BMI, and it’s implicit conclusions about currency valuations, tell us about the US consumer, US GDP growth, and, of course, the BMIs far more expensive cousin, the SHI? Let’s take look.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

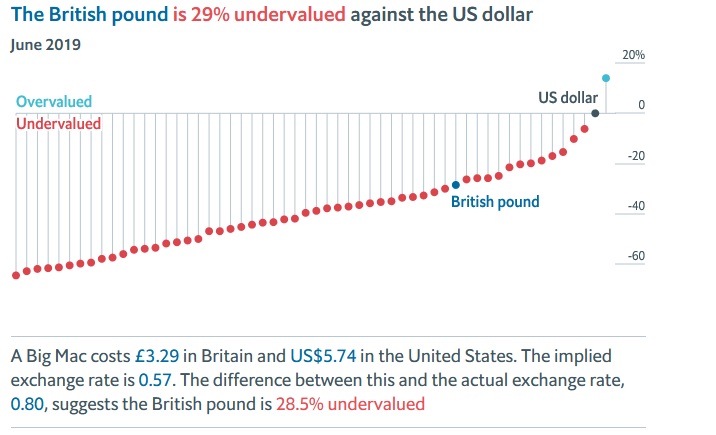

Measured with raw data, only one currency is overvalued against the US dollar. And that would be the Swiss Franc. Every other currency, of every other country, when compared to the US dollar, is undervalued. Here’s a great chart courtesy of The Economist magazine:

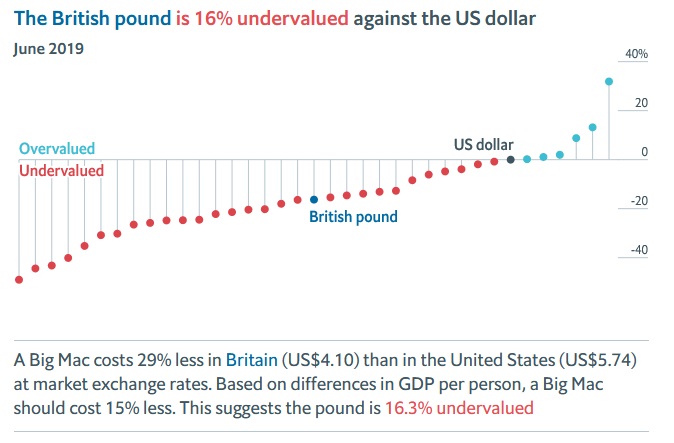

But just as beef tartare is considered dangerous by many foodies, many believe “raw” data can be a bit dangerous, too. Because in its raw form, the BMI does not account for country variances in per-capita GDP. If we adjust the data for per-person GDP, the chart is different:

In fact, once we adjust for GDP differences in these countries, it appears the currencies in Brazil, Thailand, Columbia, Canada, Chile and Sweden are overvalued against the US dollar. Of course, with the exception of Canada, we really don’t have much of a trade relationship with this list of countries.

What’s the point here? Well, for one thing, I’ve always liked the Big Mac. So, hey, if I have a chance to work it into the conversation, I will! 🙂

The second point is that through both lenses — “raw” data or per-capita GDP adjusted — the US dollar appears to overvalued. At least, as far as the Big Mac Index is concerned. Interestingly enough, President Trump seems to agree. He feels the US dollar is too strong compared to the currencies of our trading partners. I also believe he enjoys a Big Mac or two, now and then, but this fact is unconfirmed. He would probably say “that’s fake news!” Could be. 🙂

According to the BMI, the US dollar is significantly overvalued compared to our primary trading partners around the globe. How much you ask?

- 20% when compared to the euro.

- 37% when compared to the Japanese yen.

- 28% against the pound.

If the dollar is truly overvalued, then US exports are more expensive to other countries. So, when possible, these countries would reduce US products when they can purchase the same, or a similar, product from a country where their currency had more value. Further, an overvalued dollar makes US imports cheaper. So other countries find the US to be a great place to sell their goods and services. The net effect of all of this is twofold:

- downward pressure on our GDP; and,

- upward pressure on our trade deficit.

Frankly, both outcomes are very undesirable for the US. Which is why President Trump is not happy with the value of the US dollar. Nor is he happy with US interest rates vis-a-vis the short term interest rates of our trading partners. Which is one reason, I suspect, why FED Chairman Powell was asked to meet with President Trump in the past few days. Of course, once again, I could be wrong. More fake news perhaps? 🙂

Regardless, whether measured by the BMI or other metrics, the US dollar does appear expensive against other currencies. This condition makes toasters and X-mas ornaments made overseas cheap for us to purchase at Walmart, but causes sales challenges for Harley Davidson in Europe or Asia. Interestingly enough, a strong dollar has another impact on our economy: Cheap imports help prop up consumer spending. So while international trade may be hampered by a strong USD, domestic consumer spending is enhanced. Which is a good thing for our continuing economic growth. We like consumer spending!

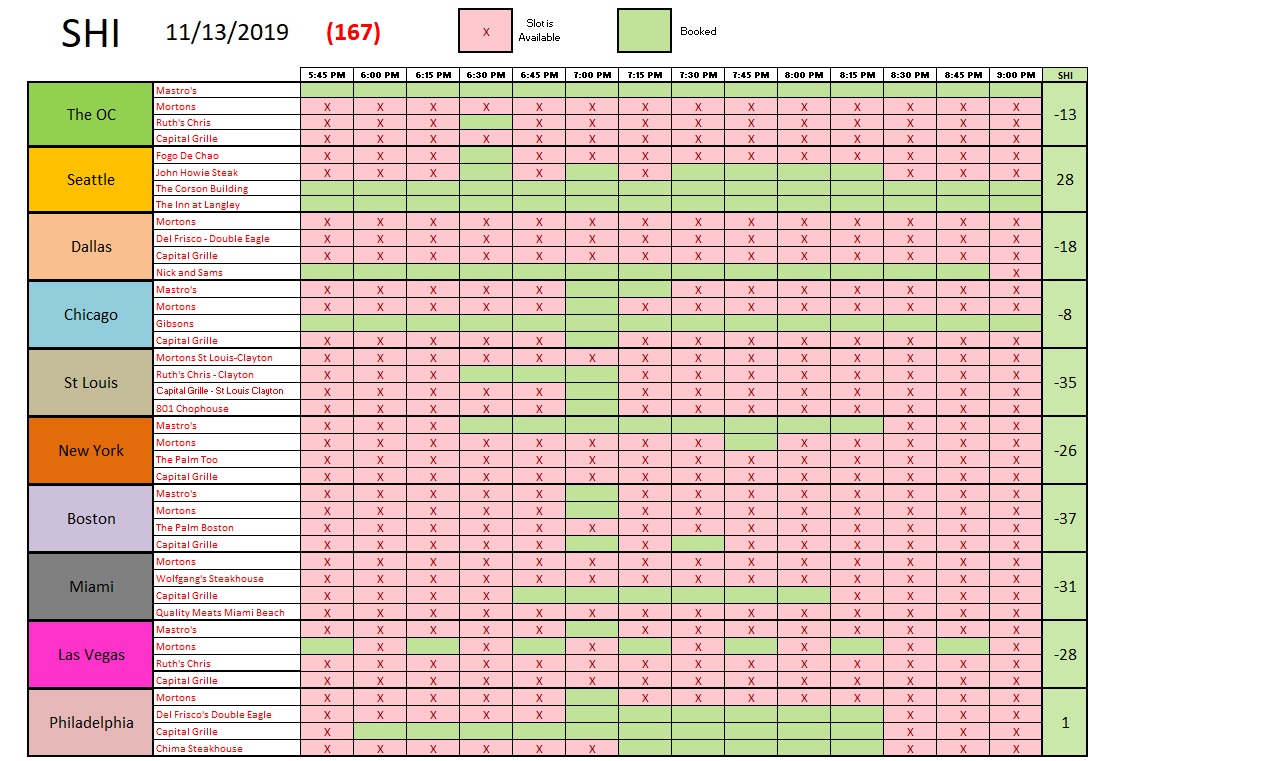

Let’s check in with the steakhouses. This week, reservation demand is a bid weaker than the prior week. Mastros continue its popularity in the OC, and a few other markets in the SHI10, but overall reservation demand for Saturday next is soft.

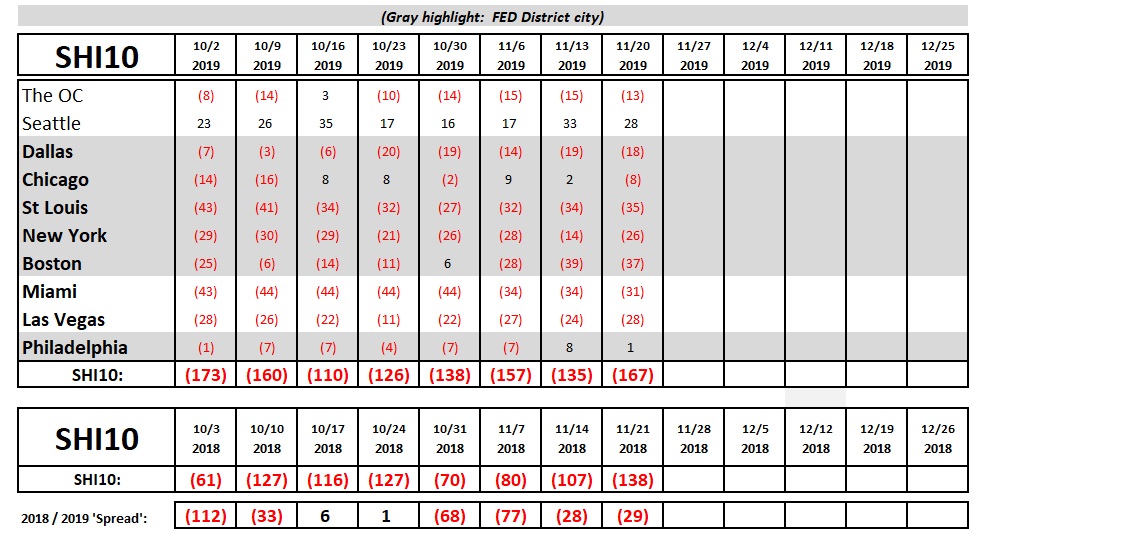

But the softness notwithstanding, we’re still on trend. When compared to the reading from one year ago, demand for reservations and expensive steaks suggests consistent consumer demand. No big changes here. All in all, our SHI10 is suggesting our economy keeps chugging along, albeit at a lower pace. Take a look:

Consistency. It’s a great thing … for tracking Big Mac prices country to country, and for forecasting GDP growth in coming quarters. Consistently measuring the quantity of pricey steakhouse reservations, on the same day of the week, at the same time of the day, week after week, permits us to make that forecast. The Atlanta FED and the NY FED follow the same rigorous methodology when they formulate their GDP forecasts, known as the ‘GDPNow’ and the ‘Nowcast’, respectively.

And what are our friends in Atlanta and New York forecasting 4th quarter GDP growth to be?

- As of yesterday, November 19th, Atlanta expects the Q4 GDP reading to be a very weak 0.4%. Ouch. https://www.frbatlanta.org/cqer/research/gdpnow

- As of November 15th, the NY FED is forecasting an identical number. 0.4% for Q3 GDP growth. Double ouch. https://www.newyorkfed.org/research/policy/nowcast

Last week I suggested our economic expansion, now over 10 years old, is sputtering along, much like a car running on 5 cylinders. The Atlanta and NY FEDs, I believe, are suggesting my forecast is too optimistic. Their forecasts suggest we’re running on 3 cylinders. Remember, Q1 GDP growth was 3.1% If Q4 measures only 0.4%, that will be a very, very weak quarterly number to end the year. And for the year, in total, that measure would give us a 1.85% growth rate for 2019. A far cry from 3%+.

I think our FED buddies might be overly pessimistic here. I think we’re doing better than that. But make no mistake: Our economy is NOT running on 8 cylinders.

- Terry Liebman