SHI 1/1/2020 – Retooling and Reflecting for a New Decade

SHI 12.18.19 – Goodbye to an Exciting Year

December 18, 2019

SHI 1/8/2020 – The Future is Looking Smaller.

January 8, 2020

“The 2020’s have begun. I decided it was time to retool.”

Not radically … but changes were needed. No one likes it when things become stale — especially food. And since this IS the Steak House Index, we must avoid stale at all costs! And so my retooling for this new decade began. Welcome to 2020 and the NEW and IMPROVED Steakhouse Index!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

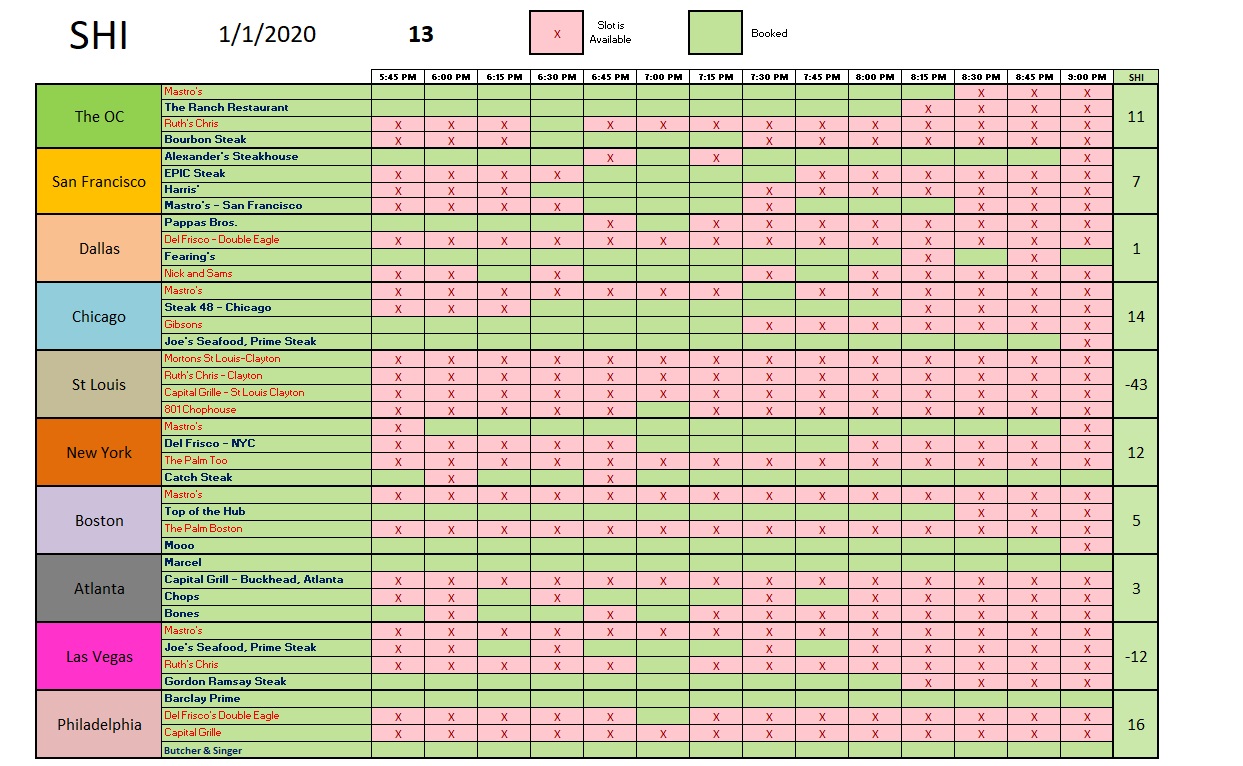

I began with Seattle. Two of our pricey steakhouses in Seattle stopped reporting table availability to OpenTable.com. When I attempted to replace those two, I discovered expensive steakhouses are not very plentiful in the city. After some serious thought and hand wringing, I decided Seattle had to go. Bye bye Seattle! No more SHI for you! But what city should take Seattle’s place? Hmmm…. I thought. And then it hit me: The Federal Reserve has 12 banks within 12 districts distributed across the US. “Why not replace Seattle with a FED bank city?,” I thought. Not only will this expand our elegant eatery choices, but increasing the alignment with the SHI10 and the FED12 makes a lot of sense. Thus, San Francisco became Seattle’s replacement.

For similar reasons, I replaced Miami with Atlanta. But also because week after week, Miami steakhouses were empty. Or close to it. As a data point, the market neither helped or hindered the SHI. It proved fairly irrelevant. I’m hoping reservation demand in pricey Atlanta steakhouses will be more dynamic. We’ll see.

I made similar changes to every other city — except St Louis. I felt we needed to see greater overall reservation demand in order to monitor possible changes in the economic winds as they occur. I’ll talk more about this next week.

Here’s the result. Notice the name of “new” restaurants in each of our 10 SHI cities (except St Louis) appear in blue.

Notice San Francisco and Atlanta? They’re on the chart.

Rest assured, I was reluctant to change the model since any change makes year-over-year comparisons a bit more difficult. So bear with me, and I’ll discuss the logic and methodology in more detail next week.

As the 2020’s begin, I find myself reflecting on the years gone by … and the future yet to come. The last century brought us a staggering number of changes, many with both epic and unknown implications in the years to come. The list includes the proliferation of the car, air travel, TV, moon landings, satellites, and — of course — the internet all quickly come to mind. And don’t forget Netflix, right? 🙂

I would have trouble compiling a list of all the amazing changes, however. I prefer to look at decades, and their global impact, thru a somewhat thematic lens:

-

The 1920s: The go-go years of the roaring ’20s. The US began to set the stage, following the staggering losses from WWI, to become the global world economic power it is today. US economic growth was as ubiquitous as the financial pain in much of Europe. But our foot-lose and fancy-free attitudes gave way to excesses, speculation, bad choices and the Crash of ’29.

-

The 1930s: The Great Depression defined this decade. The FED — less than 2-decades old, born in 1913 — struggled to overcome the massive structural deficiencies caused by what some economists now call a ‘balance sheet recession.’ (This is an interesting topic that I’ll return to in future blogs.) Fascism found a home, and began to flourish, in Europe.

-

The 1940s: The US came together behind a common purpose, to fight a common enemy. Patriotism reigned.

-

The 1950s: The American suburb was born and all over America, single family homes with a 2-car garage popped up seemingly overnight. People left the cities in droves for the space and solitude of the suburb. Right, Boomer?

-

The 1960s: A decade of innocence lost and distrust of authority and institutions. By and large, younger Americans no longer felt aligned in vision and purpose with American leadership.

-

The 1970s: Early in the decade, in part due to economic and inflationary imbalances caused by the Vietnam war, the US permanently severed its relationship with the ‘Gold Standard’ resulting in the unintended consequence of an even greater inflationary spiral. With the ascendancy and hegemony of OPEC, the great petro-inflation years began.

-

The 1980s: The new chair of the FED, Paul Volcker, decided to crush rampant and uncontrollable inflation once and for all. It took years, and was extremely painful, but the FED did the job. By the end of the decade, both inflation and interest rates were lower and in greater control. The new FED chair, Alan Greenspan, took the reins and oversaw a doubling of US GDP by the end of this turbulent decade.

-

The 1990s: As the ARPANET was dismantled, its “child”, the internet, grew, flourished, expanded and became the future.

-

The 2000s: Across the globe: Bad choices, unchecked greed, and moral hazard collectively ushered in The Great Recession.

- The 2010s: This was our recovery decade following The Great Recession. Slow and steady, our economy healed. With irrational exuberance seemingly held at bay, our economic system was able to enjoy what has now become the longest economic expansion since expansions were first measured in 1854. But the the economy showed great resilience, something else was lost: The truth. I will forever think of the 2010’s as the decade when fiction and truth became inexorably intertwined. Whether ‘fake news,’ Russian and Chinese interference in both our political and/or social networks, or our own out-of-control social media juggernauts, it’s hard to tell truth from fiction these days. Which is one of the reasons I write this blog. Facts are facts. At least I believe they are. I will always strive to share only foundational fact.

So, against this backdrop, I propose a thematic lens for the 2020’s: No one is entitled to their own set of facts. And no one articulated this concept better than the late Senator Patrick Moyinahan: “Everyone is entitled to his own opinion but not his own facts.” Here here. Well said. I will share my opinion … and you’ll know when I do. I will continue to follow the Senator’s lead as assiduously as possible. I hope other public figures join me as our new decade takes flight. Happy New Year!

– Terry Liebman